What a whirlwind of a week we have had so far! This week was full of economic data, tariffs, news headlines and big swings in both the stock and treasury markets. The Dow Jones fell over 1500 points this morning, extending losses that began after President Trump’s “Liberation Day”. The treasury market has also seen yields tumble as the 10-Year Treasury fell below 4.00% this morning, currently sitting at 3.89%, for the first time since October 2024. News from the labor market with the JOLTS Report, ADP Employment and today’s Non-Farm Payrolls/Unemployment Rate report in conjunction with data on ISM Manufacturing and ISM Services have helped push stocks and treasury yields down even further. We are also on the precipice of the NCAA March Madness Final Four, which features all #1 seeds in the tournament. The last time this happened was… 2008… Let's hope the economy turns out different this time!

Of course, the big news this week came on Wednesday afternoon, as President Trump and his administration announced their tariff plan. The following morning, financial markets across the world reacted and the U.S. stock market ultimately took the worst of it as the Dow Jones Industrial Average fell more than 1600 points in a single day. This was the largest single day decline since March 2020. Stay tuned as the Dow Jones is already trying to break that record again today. The Dollar took a hit as well, falling 1.3%, which is the sharpest decline in almost 2 years. Treasury yields also felt the impact of the tariff news. Yields were down across the board this week, as the 2-Year Treasury fell by 31bp and the 10-Year Treasury fell by 26bp. China announced retaliatory tariffs of 34% on all imported goods from the U.S., which sent stocks reeling even further this morning.

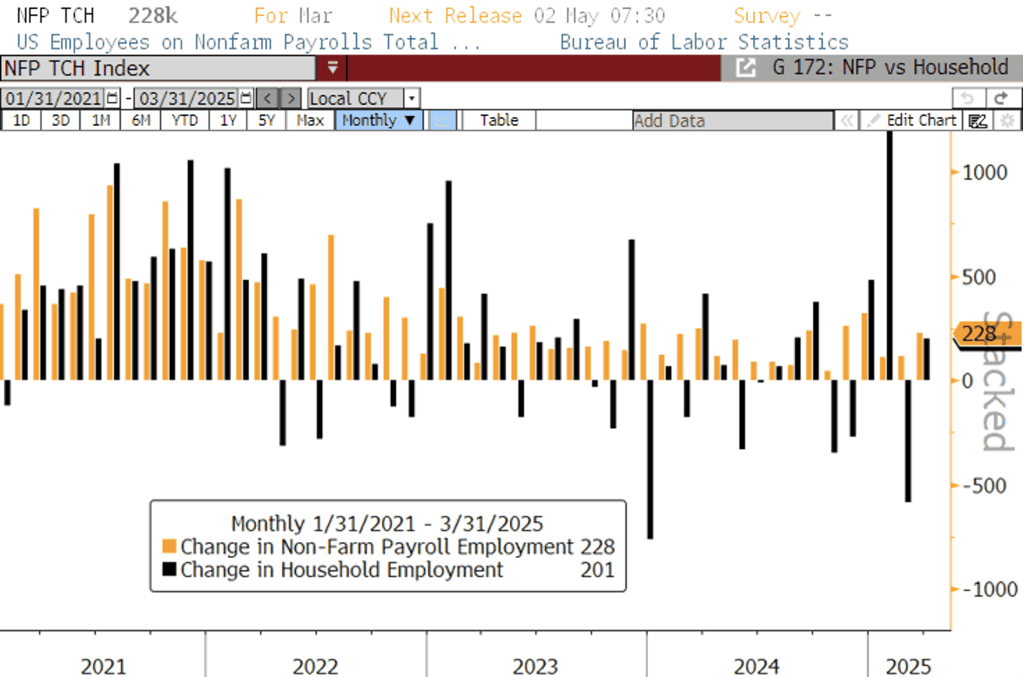

Bond yields and the stock market continued their declines this morning, despite a relatively strong jobs report that showed the economy added more jobs than expected and the unemployment rate rose as more people reentered the labor force. The March non-farm payrolls increased by 228k versus as estimate of 140k. The gains in the non-farm payroll figure were relatively broad-based, with health care & social assistance (+78k) and leisure & hospitality (+43k) leading the charge. The previous two months were revised lower by a combined 48k. The unemployment rate rose for the second consecutive month to 4.2% versus the estimate of 4.1% as more people reentered the labor force, raising the labor force participation rate to 62.5%.

The Federal Funds Futures Market is currently pricing in a full rate cut at the June meeting, and just over 4 by the end of 2025. Today’s strong jobs report could make rate cuts more difficult, as it would take a further deterioration in the labor market before the FOMC would decide on a cut in their target rate. There is still a lot of data to come in and digest before the FOMC’s next meeting in May, including another jobs report, March CPI and PCE and Q1 2025 GDP. At the end of this month, the U.S. Bureau of Economic Analysis (BEA) will release their first print on GDP for Q1 2025. The Atlanta Fed’s GDP Now model is currently estimating a print of -2.8%, driven by a downturn in growth projections and consumer spending.

Next week brings an updated print on Wholesale Inventories, CPI, PPI and the University of Michigan Consumer Sentiment Survey. It also brings an amazing week in sports as the NCAA Basketball National Championship will finish on Monday and the Masters beings on Thursday. Have a wonderful weekend everybody!

The Baker Group is one of the nation’s largest independently owned securities firms specializing in investment portfolio management for community financial institutions.

Since 1979, we’ve helped our clients improve decision-making, manage interest rate risk, and maximize investment portfolio performance. Our proven approach of total resource integration utilizes software and products developed by Baker’s Software Solutions* combined with the firm’s investment experience and advice.

Author

Luke Mikles

Senior Vice President, Financial Strategies Group

The Baker Group LP

800.937.2257

*The Baker Group LP is the sole authorized distributor for the products and services developed and provided by The Baker Group Software Solutions, Inc.

INTENDED FOR USE BY INSTITUTIONAL INVESTORS ONLY. Any data provided herein is for informational purposes only and is intended solely for the private use of the reader. Although information contained herein is believed to be from reliable sources, The Baker Group LP does not guarantee its completeness or accuracy. Opinions constitute our judgment and are subject to change without notice. The instruments and strategies discussed here may fluctuate in price or value and may not be suitable for all investors; any doubt should be discussed with a Baker representative. Past performance is not indicative of future results. Changes in rates may have an adverse effect on the value of investments. This material is not intended as an offer or solicitation for the purchase or sale of any financial instruments.